ogc163

Superstar

In 1788, George Washington predicted that America would be “the most favorable country of any in the world for persons of industry and frugality,” ideal for even those in the lowest social classes to immigrate to, given “the equal distribution of property, the great plenty of unoccupied lands, and the facility of procuring the means of subsistence.” Opportunity, he argued, was inherent in its vast lands and religious tolerance.

In 2016, 228 years later, Alex Zhu, the co-CEO of Musical.ly and later VP of product at Bytedance, echoed these sentiments in the context of starting a new social network. Launching a new platform, he said, was like starting a new country: Getting users to move from an established network that had an ossified economy and social classes to a new network requires the possibility of success—the lure of the American Dream. Furthermore, the new social network had to create upward mobility for all users, to “make sure there’s a middle class coming up.”

On most content platforms today, the ethos of the American Dream is alive and well—a recent study of kids ages eight to 12 found that nearly 30% aspire to become YouTubers. With countless examples of normal people achieving massive success on the platform, this should come as no surprise. Just last year, YouTube creator David Dobrik’s monthly AdSense checks from the platform were $275,000 for an average of 60 million views. On Substack, the top 10 creators are collectively bringing in more than $7 million annually. Charli D’Amelio—who recently became the first TikTok creator to surpass 100 million followers—is estimated to be worth $4 million at age 16. She started on TikTok just 1.5 years ago.

But while some have been propelled to massive stardom, examples of a wide swath of the population achieving financial security from these platforms are few and far between. The current creator landscape more closely resembles an economy in which wealth is concentrated at the top. On Patreon, only 2% of creators made the federal minimum wage of $1,160 per month in 2017. On Spotify, artists need 3.5 million streams per year to achieve the annual earnings for a full-time minimum-wage worker of $15,080, a fact that drives most musicians to supplement their earnings with touring and merchandise. In contrast, in America in 2016, 52% of adults lived in middle income households, with incomes ranging from $48,500 to $145,500.

The missing creator middle class

The sustainability of nations and the defensibility of platforms is better when wealth isn’t concentrated in the top 1%. In the real world, a healthy middle class is critical for promoting societal trust, providing a stable source of demand for products and services, and driving innovation. On platforms, less wealth concentration means lessening the risk that a would-be competitor could poach top creators and threaten the entire business.

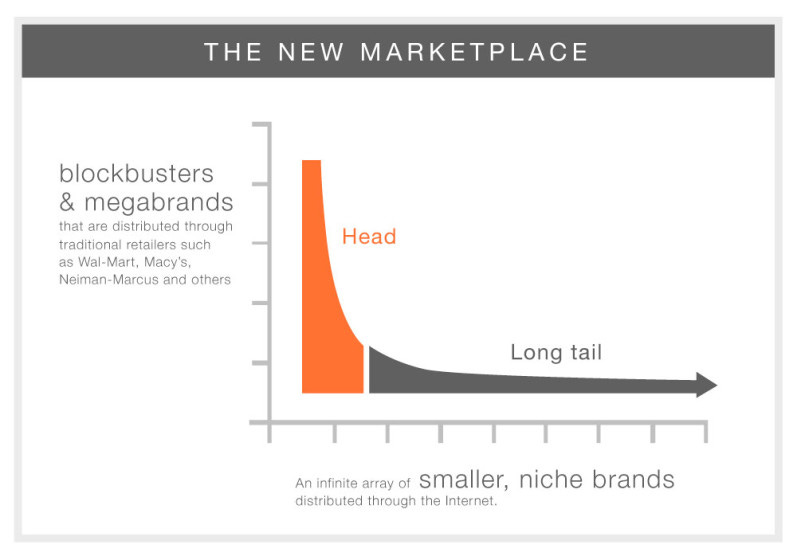

Ever since Wired magazine editor Chris Anderson first published his “Long Tail” theory in 2004, the idea has been endlessly reinforced, contradicted, and debated. He argued that the internet’s removal of physical limitations (local audiences, scarce shelf space) would empower niche products and creators to flourish.

In the search category, the phenomenon has proven true: Google has revealed that on a daily basis, 15% of all queries have never been searched before, a figure that has remained stable since 2013.

But for content platforms, the move to digital content hasn’t been correlated with a burgeoning long tail: the top creators are massively successful, while long-tail creators are barely getting by. On Spotify, for instance, the top 43,000 artists—roughly 1.4% of those on the platform—pull in 90% of royalties and make, on average, $22,395 per artist per quarter. The rest of its 3 million creators, or 98.6% of its artists, made just $36 per artist per quarter.

Even in the video gaming world, signs point to success being increasingly concentrated among a smaller number of game creators. An essay by Electronic Arts product lead Ran Mo points out that on the online gaming platform Roblox, concentration at the top has increased even as total usage has grown: In 2018, the top game on Roblox accounted for 8 to 10% of concurrent users, while in 2020, the top game accounts for upwards of 20 to 25% of concurrent users. He proposes two reasons for this concentration: the lack of an upper limit for engagement in games, and the social nature of games leading to winner-take-all network effects.

A 1981 paper by Sherwin Rosen, an economist at the University of Chicago, offers a prescient explanation of how the “superstar phenomenon” would become more pronounced as a result of technology. Rosen argued that in markets with heterogeneous providers, like most creator economies, success accrues disproportionately to those on top: “lesser talent often is a poor substitute for greater talent [...] hearing a succession of mediocre singers does not add up to a single outstanding performance.” This phenomenon is further exacerbated by technology which lowers distribution costs: the best performers in a given field are freed from physical constraints like the size of concert halls—and can address an unlimited market and reap a greater share of revenue.

So, is inequality inevitable among creators? Perhaps to an extent. Not everyone can become a celebrity, but there are examples of middle-class creators: those that aren’t household names but have a solid base of customers who provide the foundation for a decent income.

What is certainly true is this: Creator platforms flourish when they provide opportunity for anyone to grow and succeed. When the American Dream is just a dream, the fate of platforms becomes precarious. Vine serves as a cautionary tale: Despite inventing the short-form comedy video format and reaching 200 million monthly active users in November 2015, the company gradually lost its creators to platforms like Instagram, YouTube, and Snap, where they could earn more, build bigger audiences, and have a wider range of creative tools. Opportunities for audience growth and financial success were more readily available on other platforms, contributing to the platform’s decline.

The Charlis and Addisons will always emerge and exist, but it’s vital for creator platforms to provide paths for upward mobility and democratize opportunities to succeed. How can platforms do this?

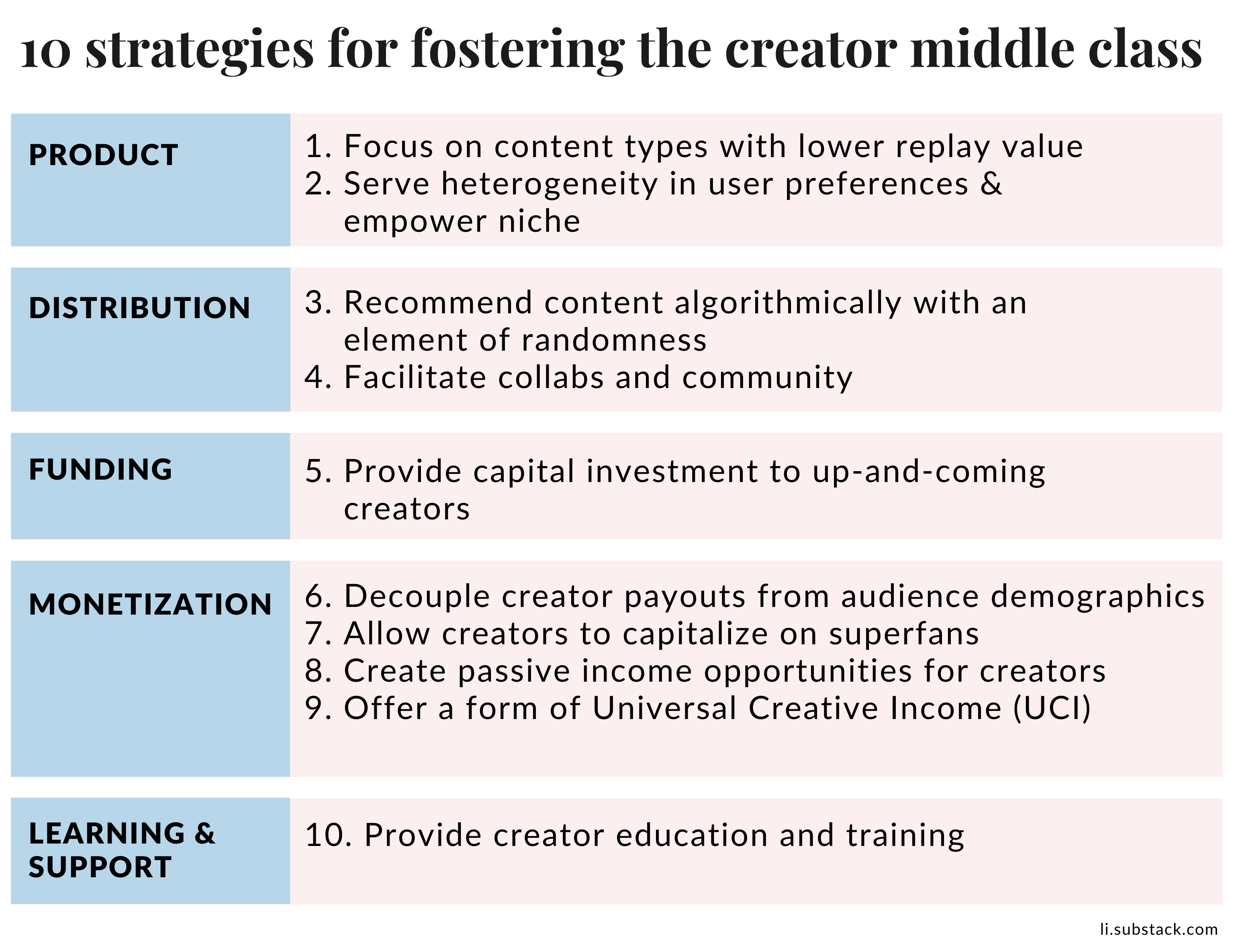

10 strategies to grow the middle class of creators

The middle class in America didn’t just happen naturally, but was born of 20th-century policies that created widespread prosperity: Roosevelt’s New Deal; the Fair Labor Standards Act, which established the minimum wage, overtime pay, and prohibition of employment of minors; a rise in unionism; the passage of the GI Bill; and the creation of the Federal Housing Administration. These policies shifted the balance of power to workers, distributed opportunity for wealth creation, and mitigated growing income inequality, helping to build a strong middle class that comprised 61% of American adults by the end of the 1960s. As policy priorities shifted, that number shrank to 51% in 2019.

Platforms, too, can make decisions that affect their own economies. Some inequality is inherent in the nature of the passion economy: supply is heterogeneous and non-substitutable, and the trust and affinity that creators build with their audiences should be celebrated. But platforms—from established to brand new—can do more to strengthen the creator middle class and broaden the path to success. What are some platform design decisions that can help make success attainable by many?

In 2016, 228 years later, Alex Zhu, the co-CEO of Musical.ly and later VP of product at Bytedance, echoed these sentiments in the context of starting a new social network. Launching a new platform, he said, was like starting a new country: Getting users to move from an established network that had an ossified economy and social classes to a new network requires the possibility of success—the lure of the American Dream. Furthermore, the new social network had to create upward mobility for all users, to “make sure there’s a middle class coming up.”

On most content platforms today, the ethos of the American Dream is alive and well—a recent study of kids ages eight to 12 found that nearly 30% aspire to become YouTubers. With countless examples of normal people achieving massive success on the platform, this should come as no surprise. Just last year, YouTube creator David Dobrik’s monthly AdSense checks from the platform were $275,000 for an average of 60 million views. On Substack, the top 10 creators are collectively bringing in more than $7 million annually. Charli D’Amelio—who recently became the first TikTok creator to surpass 100 million followers—is estimated to be worth $4 million at age 16. She started on TikTok just 1.5 years ago.

But while some have been propelled to massive stardom, examples of a wide swath of the population achieving financial security from these platforms are few and far between. The current creator landscape more closely resembles an economy in which wealth is concentrated at the top. On Patreon, only 2% of creators made the federal minimum wage of $1,160 per month in 2017. On Spotify, artists need 3.5 million streams per year to achieve the annual earnings for a full-time minimum-wage worker of $15,080, a fact that drives most musicians to supplement their earnings with touring and merchandise. In contrast, in America in 2016, 52% of adults lived in middle income households, with incomes ranging from $48,500 to $145,500.

The missing creator middle class

The sustainability of nations and the defensibility of platforms is better when wealth isn’t concentrated in the top 1%. In the real world, a healthy middle class is critical for promoting societal trust, providing a stable source of demand for products and services, and driving innovation. On platforms, less wealth concentration means lessening the risk that a would-be competitor could poach top creators and threaten the entire business.

Ever since Wired magazine editor Chris Anderson first published his “Long Tail” theory in 2004, the idea has been endlessly reinforced, contradicted, and debated. He argued that the internet’s removal of physical limitations (local audiences, scarce shelf space) would empower niche products and creators to flourish.

In the search category, the phenomenon has proven true: Google has revealed that on a daily basis, 15% of all queries have never been searched before, a figure that has remained stable since 2013.

But for content platforms, the move to digital content hasn’t been correlated with a burgeoning long tail: the top creators are massively successful, while long-tail creators are barely getting by. On Spotify, for instance, the top 43,000 artists—roughly 1.4% of those on the platform—pull in 90% of royalties and make, on average, $22,395 per artist per quarter. The rest of its 3 million creators, or 98.6% of its artists, made just $36 per artist per quarter.

Even in the video gaming world, signs point to success being increasingly concentrated among a smaller number of game creators. An essay by Electronic Arts product lead Ran Mo points out that on the online gaming platform Roblox, concentration at the top has increased even as total usage has grown: In 2018, the top game on Roblox accounted for 8 to 10% of concurrent users, while in 2020, the top game accounts for upwards of 20 to 25% of concurrent users. He proposes two reasons for this concentration: the lack of an upper limit for engagement in games, and the social nature of games leading to winner-take-all network effects.

A 1981 paper by Sherwin Rosen, an economist at the University of Chicago, offers a prescient explanation of how the “superstar phenomenon” would become more pronounced as a result of technology. Rosen argued that in markets with heterogeneous providers, like most creator economies, success accrues disproportionately to those on top: “lesser talent often is a poor substitute for greater talent [...] hearing a succession of mediocre singers does not add up to a single outstanding performance.” This phenomenon is further exacerbated by technology which lowers distribution costs: the best performers in a given field are freed from physical constraints like the size of concert halls—and can address an unlimited market and reap a greater share of revenue.

So, is inequality inevitable among creators? Perhaps to an extent. Not everyone can become a celebrity, but there are examples of middle-class creators: those that aren’t household names but have a solid base of customers who provide the foundation for a decent income.

What is certainly true is this: Creator platforms flourish when they provide opportunity for anyone to grow and succeed. When the American Dream is just a dream, the fate of platforms becomes precarious. Vine serves as a cautionary tale: Despite inventing the short-form comedy video format and reaching 200 million monthly active users in November 2015, the company gradually lost its creators to platforms like Instagram, YouTube, and Snap, where they could earn more, build bigger audiences, and have a wider range of creative tools. Opportunities for audience growth and financial success were more readily available on other platforms, contributing to the platform’s decline.

The Charlis and Addisons will always emerge and exist, but it’s vital for creator platforms to provide paths for upward mobility and democratize opportunities to succeed. How can platforms do this?

10 strategies to grow the middle class of creators

The middle class in America didn’t just happen naturally, but was born of 20th-century policies that created widespread prosperity: Roosevelt’s New Deal; the Fair Labor Standards Act, which established the minimum wage, overtime pay, and prohibition of employment of minors; a rise in unionism; the passage of the GI Bill; and the creation of the Federal Housing Administration. These policies shifted the balance of power to workers, distributed opportunity for wealth creation, and mitigated growing income inequality, helping to build a strong middle class that comprised 61% of American adults by the end of the 1960s. As policy priorities shifted, that number shrank to 51% in 2019.

Platforms, too, can make decisions that affect their own economies. Some inequality is inherent in the nature of the passion economy: supply is heterogeneous and non-substitutable, and the trust and affinity that creators build with their audiences should be celebrated. But platforms—from established to brand new—can do more to strengthen the creator middle class and broaden the path to success. What are some platform design decisions that can help make success attainable by many?