MrSinnister

Delete account when possible.

Keynesian economics

Page issues

Keynesian economics (/ˈkeɪnziən/ kayn-zee-ən; or Keynesianism) are the various theories about how in the short run, and especially during recessions, economic output is strongly influenced by aggregate demand(total spending in the economy). In the Keynesian view, aggregate demand does not necessarily equal the productive capacity of the economy; instead, it is influenced by a host of factors and sometimes behaves erratically, affecting production, employment, and inflation.[1][2]

The theories forming the basis of Keynesian economics were first presented by the British economist John Maynard Keynes in his book,The General Theory of Employment, Interest and Money, published in 1936, during theGreat Depression. Keynes contrasted his approach to the aggregate supply-focused 'classical' economics that preceded his book. The interpretations of Keynes that followed are contentious and several schools of economic thought claim his legacy.

Keynesian economists often argue thatprivate sector decisions sometimes lead to inefficient macroeconomic outcomes which require active policy responses by the public sector, in particular, monetary policy actions by the central bank and fiscal policy actions by the government, in order to stabilize output over the business cycle.[3] Keynesian economics advocates a mixed economy – predominantly private sector, but with a role for government intervention during recessions.

Keynesian economics served as the standard economic model in the developed nationsduring the later part of the Great Depression,World War II, and the post-war economic expansion (1945–1973), though it lost some influence following the oil shock and resultingstagflation of the 1970s.[4] The advent of thefinancial crisis of 2007–08 caused aresurgence in Keynesian thought,[5] which continues as new Keynesian economics.

Historical context

TheoryEdit

Keynes argued that the solution to the Great Depression was to stimulate the economy ("inducement to invest") through some combination of two approaches:

Expansionary fiscal policy consists of increasing net public spending, which the government can effect by a) taxing less, b) spending more, or c) both. Investment and consumption by government raises demand for businesses' products and for employment, reversing the effects of the aforementioned imbalance.[1] If desired spending exceeds revenue, the government finance the difference by borrowing from capital marketsby issuing government bonds. This is called deficit spending. Two points are important to note at this point. First, deficits are not required for expansionary monetary policy, and second, it is only change in net spending that can stimulate or depress the economy. For example, if a government ran a deficit of 10% both last year and this year, this would represent neutral fiscal policy. In fact, if it ran a deficit of 10% last year and 5% this year, this would actually be contractionary. On the other hand, if the government ran a surplus of 10% of GDP last year and 5% this year, that would be expansionary fiscal policy, despite never running a deficit at all.

In the price mechanism of neoclassical economics, it is predicted that, in a competitive market, if demand for a particular good or service falls, that would immediately cause the price for that good or service to fall, which in turn would decrease supply and increase demand, thereby bringing them back to equilibrium. A central conclusion of Keynesian economics, in strong contrast to the previously dominant models ofneoclassical synthesis, is that there are some situations in which a depressed economy would not quickly self-correct towards full employment and potential output, but could remain trapped indefinitely with both high unemployment and mothballed factories. To the observation that these were, in fact, the prevailing conditions throughout the industrialized world for many years during the Great Depression, classical models could only conclude that it was a temporary aberration. The purpose of Keynes' theory was to show such conditions could, without intervention, persist in a stable, though dismal, equilibrium.

By the end of the Second World War, Keynesianism was the most popular school of economic theory in the non-Communist world. Beginning in the late 1960s, a new classical macroeconomics movement arose, critical of Keynesian assumptions (see sticky prices), and seemed, especially in the 1970s, to explain certain phenomena (e.g. the co-existence of high unemployment and high inflation, or "stagflation") better. It was characterised by explicit and rigorous adherence to microfoundations, as well as use of increasingly sophisticated mathematical modeling. However, by the late 1980s, certain failures of the new classical models, both theoretical (see Real business cycle theory) and empirical (see the "Volcker recession")[8] hastened the emergence of New Keynesian economics, a school which sought to unite the most realistic aspects of Keynesian and neo-classical assumptions and place them on more rigorous theoretical foundation than ever before.

Interpretations of Keynes have emphasized his stress on the international coordination of Keynesian policies, the need for international economic institutions, and the ways in which economic forces could lead to war or could promote peace.[9]

ConceptEdit

Wages and spendingEdit

During the Great Depression, the classical theory attributed mass unemployment to high and rigid real wages.[citation needed]

To Keynes, the determination of wages was more complicated. First, he argued that it is not real but nominal wages that are set in negotiations between employers and workers, as opposed to a barter relationship. Second, nominal wage cuts would be difficult to put into effect because of laws and wage contracts. Even classical economists admitted that these exist; unlike Keynes, they advocated abolishing minimum wages, unions, and long-term contracts, increasinglabour market flexibility. However, to Keynes, people will resist nominal wage reductions, even without unions, until they see other wages falling and a general fall of prices.

Keynes rejected the idea that cutting wages would cure recessions. He examined the explanations for this idea and found them all faulty. He also considered the most likely consequences of cutting wages in recessions, under various different circumstances. He concluded that such wage cutting would be more likely to make recessions worse rather than better.[10]

Further, if wages and prices were falling, people would start to expect them to fall. This could make the economy spiral downward as those who had money would simply wait as falling prices made it more valuable – rather than spending. As Irving Fisher argued in 1933, in his Debt-Deflation Theory of Great Depressions, deflation (falling prices) can make a depression deeper as falling prices and wages made pre-existing nominal debts more valuable in real terms.

Excessive savingEdit

To Keynes, excessive saving, i.e. saving beyond planned investment, was a serious problem, encouraging recession or evendepression. Excessive saving results if investment falls, perhaps due to falling consumer demand, over-investment in earlier years, or pessimistic business expectations, and if saving does not immediately fall in step, the economy would decline.

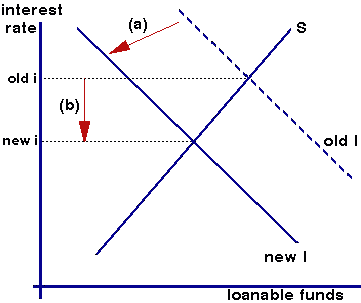

The classical economists argued that interest rates would fall due to an increase in savings. The first diagram, adapted from the only graph in The General Theory, shows this process. (For simplicity, other sources of the demand for or supply of savings are ignored here.) Assume that fixed investment in capital goods falls from "old I" to "new I" (step a). Second (step b), the resulting excess of saving causes interest-rate cuts, abolishing the excess supply: so again we have saving (S) equal to investment. The interest-rate (i) fall prevents that of production and employment.

Keynes had a complex argument against thislaissez-faire response. The graph below summarizes his argument, assuming again that fixed investment falls (step A). First, saving does not fall much as interest rates fall, since the income and substitution effectsof falling rates go in conflicting directions.Second, since planned fixed investment in plant and equipment is based mostly on long-term expectations of future profitability, that spending does not rise much as interest rates fall.

Page issues

Keynesian economics (/ˈkeɪnziən/ kayn-zee-ən; or Keynesianism) are the various theories about how in the short run, and especially during recessions, economic output is strongly influenced by aggregate demand(total spending in the economy). In the Keynesian view, aggregate demand does not necessarily equal the productive capacity of the economy; instead, it is influenced by a host of factors and sometimes behaves erratically, affecting production, employment, and inflation.[1][2]

The theories forming the basis of Keynesian economics were first presented by the British economist John Maynard Keynes in his book,The General Theory of Employment, Interest and Money, published in 1936, during theGreat Depression. Keynes contrasted his approach to the aggregate supply-focused 'classical' economics that preceded his book. The interpretations of Keynes that followed are contentious and several schools of economic thought claim his legacy.

Keynesian economists often argue thatprivate sector decisions sometimes lead to inefficient macroeconomic outcomes which require active policy responses by the public sector, in particular, monetary policy actions by the central bank and fiscal policy actions by the government, in order to stabilize output over the business cycle.[3] Keynesian economics advocates a mixed economy – predominantly private sector, but with a role for government intervention during recessions.

Keynesian economics served as the standard economic model in the developed nationsduring the later part of the Great Depression,World War II, and the post-war economic expansion (1945–1973), though it lost some influence following the oil shock and resultingstagflation of the 1970s.[4] The advent of thefinancial crisis of 2007–08 caused aresurgence in Keynesian thought,[5] which continues as new Keynesian economics.

Historical context

TheoryEdit

Keynes argued that the solution to the Great Depression was to stimulate the economy ("inducement to invest") through some combination of two approaches:

- A reduction in interest rates (monetary policy), and

- Government investment in infrastructure (fiscal policy).'

Expansionary fiscal policy consists of increasing net public spending, which the government can effect by a) taxing less, b) spending more, or c) both. Investment and consumption by government raises demand for businesses' products and for employment, reversing the effects of the aforementioned imbalance.[1] If desired spending exceeds revenue, the government finance the difference by borrowing from capital marketsby issuing government bonds. This is called deficit spending. Two points are important to note at this point. First, deficits are not required for expansionary monetary policy, and second, it is only change in net spending that can stimulate or depress the economy. For example, if a government ran a deficit of 10% both last year and this year, this would represent neutral fiscal policy. In fact, if it ran a deficit of 10% last year and 5% this year, this would actually be contractionary. On the other hand, if the government ran a surplus of 10% of GDP last year and 5% this year, that would be expansionary fiscal policy, despite never running a deficit at all.

In the price mechanism of neoclassical economics, it is predicted that, in a competitive market, if demand for a particular good or service falls, that would immediately cause the price for that good or service to fall, which in turn would decrease supply and increase demand, thereby bringing them back to equilibrium. A central conclusion of Keynesian economics, in strong contrast to the previously dominant models ofneoclassical synthesis, is that there are some situations in which a depressed economy would not quickly self-correct towards full employment and potential output, but could remain trapped indefinitely with both high unemployment and mothballed factories. To the observation that these were, in fact, the prevailing conditions throughout the industrialized world for many years during the Great Depression, classical models could only conclude that it was a temporary aberration. The purpose of Keynes' theory was to show such conditions could, without intervention, persist in a stable, though dismal, equilibrium.

By the end of the Second World War, Keynesianism was the most popular school of economic theory in the non-Communist world. Beginning in the late 1960s, a new classical macroeconomics movement arose, critical of Keynesian assumptions (see sticky prices), and seemed, especially in the 1970s, to explain certain phenomena (e.g. the co-existence of high unemployment and high inflation, or "stagflation") better. It was characterised by explicit and rigorous adherence to microfoundations, as well as use of increasingly sophisticated mathematical modeling. However, by the late 1980s, certain failures of the new classical models, both theoretical (see Real business cycle theory) and empirical (see the "Volcker recession")[8] hastened the emergence of New Keynesian economics, a school which sought to unite the most realistic aspects of Keynesian and neo-classical assumptions and place them on more rigorous theoretical foundation than ever before.

Interpretations of Keynes have emphasized his stress on the international coordination of Keynesian policies, the need for international economic institutions, and the ways in which economic forces could lead to war or could promote peace.[9]

ConceptEdit

Wages and spendingEdit

During the Great Depression, the classical theory attributed mass unemployment to high and rigid real wages.[citation needed]

To Keynes, the determination of wages was more complicated. First, he argued that it is not real but nominal wages that are set in negotiations between employers and workers, as opposed to a barter relationship. Second, nominal wage cuts would be difficult to put into effect because of laws and wage contracts. Even classical economists admitted that these exist; unlike Keynes, they advocated abolishing minimum wages, unions, and long-term contracts, increasinglabour market flexibility. However, to Keynes, people will resist nominal wage reductions, even without unions, until they see other wages falling and a general fall of prices.

Keynes rejected the idea that cutting wages would cure recessions. He examined the explanations for this idea and found them all faulty. He also considered the most likely consequences of cutting wages in recessions, under various different circumstances. He concluded that such wage cutting would be more likely to make recessions worse rather than better.[10]

Further, if wages and prices were falling, people would start to expect them to fall. This could make the economy spiral downward as those who had money would simply wait as falling prices made it more valuable – rather than spending. As Irving Fisher argued in 1933, in his Debt-Deflation Theory of Great Depressions, deflation (falling prices) can make a depression deeper as falling prices and wages made pre-existing nominal debts more valuable in real terms.

Excessive savingEdit

To Keynes, excessive saving, i.e. saving beyond planned investment, was a serious problem, encouraging recession or evendepression. Excessive saving results if investment falls, perhaps due to falling consumer demand, over-investment in earlier years, or pessimistic business expectations, and if saving does not immediately fall in step, the economy would decline.

The classical economists argued that interest rates would fall due to an increase in savings. The first diagram, adapted from the only graph in The General Theory, shows this process. (For simplicity, other sources of the demand for or supply of savings are ignored here.) Assume that fixed investment in capital goods falls from "old I" to "new I" (step a). Second (step b), the resulting excess of saving causes interest-rate cuts, abolishing the excess supply: so again we have saving (S) equal to investment. The interest-rate (i) fall prevents that of production and employment.

Keynes had a complex argument against thislaissez-faire response. The graph below summarizes his argument, assuming again that fixed investment falls (step A). First, saving does not fall much as interest rates fall, since the income and substitution effectsof falling rates go in conflicting directions.Second, since planned fixed investment in plant and equipment is based mostly on long-term expectations of future profitability, that spending does not rise much as interest rates fall.