ogc163

Superstar

TLDR:

The markets have become too hot to handle. So intense is the frenzied stock-buying that even many of Wall Street’s biggest brokerages and wealth managers are struggling to keep up.

Almost every major US brokerage firm — from old stalwarts like Charles Schwab and Merrill Lynch to new platforms such as Robinhood — suffered at least one outage in November, according to Downdetector, a website that tracks online service problems, as a torrent of trading overwhelmed their websites.

Thomas Peterffy, the billionaire founder of Interactive Brokers, who first started trading on the now-defunct American Stock Exchange in the 1970s, says the current environment is unlike anything he has ever seen before — but understandable. “Money is now so easy, why not borrow what you can and put it into stocks? That’s what our customers are doing, and they’re making helluva lot of money,” he says.

Retail investors led the dramatic equity market recovery from the Covid-19 shock, flooding internet message boards to share memes, boast of wins and lament losses. But now they are increasingly joined by the investment industry’s heavyweights, which are helping reinforce and broaden out the most remarkable bull run in financial history.

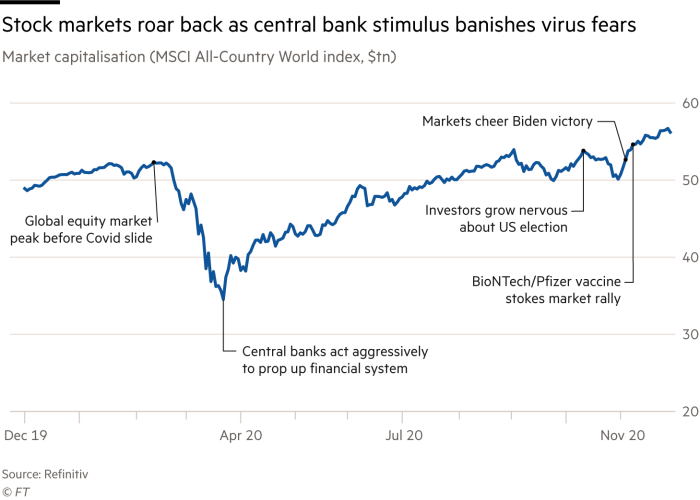

The MSCI All-Country World index climbed another 12.2 per cent in November — its best month on record — to touch new all-time highs. The gauge has added $30tn in market capitalisation since the March lows.

Moreover, this stage of the rally has been mainly powered by corners of the market largely left behind during the pandemic, such as energy stocks, airlines, hotel groups, European banks, smaller US companies and emerging markets. Indeed, it has become what some analysts have termed an “everything rally”, with junk bonds, copper, oil and even bitcoin climbing sharply. The only major markets to have taken a hit are classic havens, such as US Treasuries and gold.

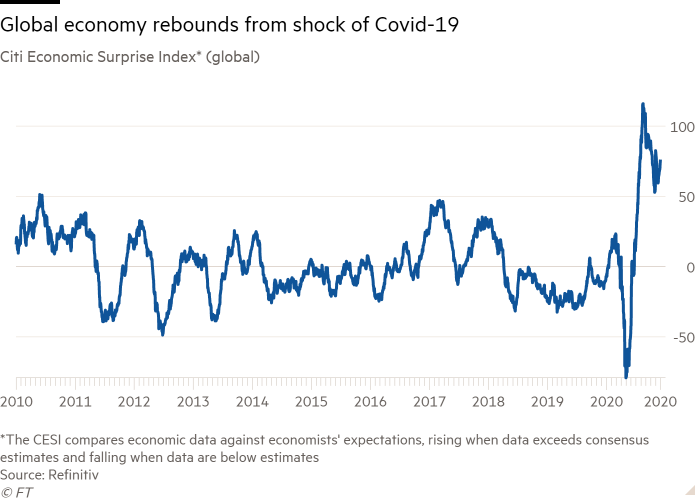

The backdrop to such a frenzy seems improbable. The second coronavirus wave is unravelling some of the tentative economic recovery from the brutal March shock. All told, the global economy is likely to shrink 4.4 per cent this year, according to the IMF — a decline not seen since the Great Depression.

However, the emergence of several credible, effective coronavirus vaccines has triggered a burst of optimism that the global economy is poised for a powerful rebound in 2021, as the pandemic recedes but the extraordinarily aggressive stimulus measures continue to send money sloshing around the financial system.

“The game-changer was the vaccine,” says Peter Oppenheimer, chief global equity strategist at Goldman Sachs. “Hope is one thing, actually seeing the evidence (of a vaccine) is quite another. And the evidence was much better than most people were expecting. We’re still optimistic that you’ll see quite good returns in equity markets next year.”

However, some investors and analysts remain uneasy about the current ebullience. Yes, effective vaccines could eventually suppress Covid-19, but for now it continues to linger and the monstrous damage it has already inflicted will take a long time to heal.

Noting signs of uncritical optimism among fund managers, Bank of America’s chief investment strategist Michael Hartnett recommends that investors ratchet back their exposure to stocks in the coming weeks and months, arguing markets are now approaching a “full bull” stage and are vulnerable to a setback.

Jeremy Grantham, the famed contrarian founder of the investment group GMO, thinks even this is optimistic. He reckons markets have smashed past the “full bull” stage and are in a late-bubble “melt-up” phase that rivals the two biggest bubbles of the past century.

“There is as much craziness now as there was in late 1999 or 1929,” he argues. “It is bewildering, impressive and for financial historians like me, exciting. This is the real thing . . . It looked like we were in a bubble mode this summer, but the real craziness has come out in the last few months.”

Magic wands

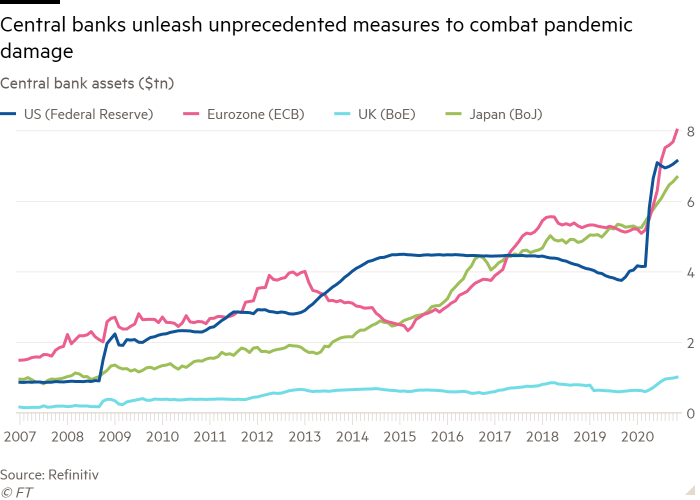

The early stage of the rally was powered by mammoth fiscal and monetary stimulus packages from central banks and governments around the world, totalling trillions of dollars. The impact of ultra-easy monetary policy including very low interest rates — and the prospect of it continuing for years to come — remains the dominant driver, analysts say.

But November’s shift from optimism to near-euphoria has been triggered by an alignment of several stars. First, Joe Biden won the US presidency but Democrats failed to gain control of the Senate. For many investors that was close to the perfect result, ejecting the erratic, norm-shattering Donald Trump but stymieing the more radical parts of the Democratic agenda — such as heavy corporate tax increases.

While another big dose of fiscal stimulus may be trickier to pass, this will mean that the Federal Reserve is more likely to keep its foot on the monetary pedal. “Gridlock is Goldilocks,” was the pithy title of one Wall Street analyst’s note on the subject. That President Donald Trump’s refusal to accept the result has failed to trigger any significant unrest has added to investors’ relief.

Then, BioNTech-Pfizer, Moderna and Oxford university-AstraZeneca announced that they had developed coronavirus vaccines that were in most cases more effective than expected. This provided an enormous jolt to global markets, which could contemplate a gradual economic normalisation next year, with pent-up demand and super-easy monetary policy fuelling a huge growth spurt.

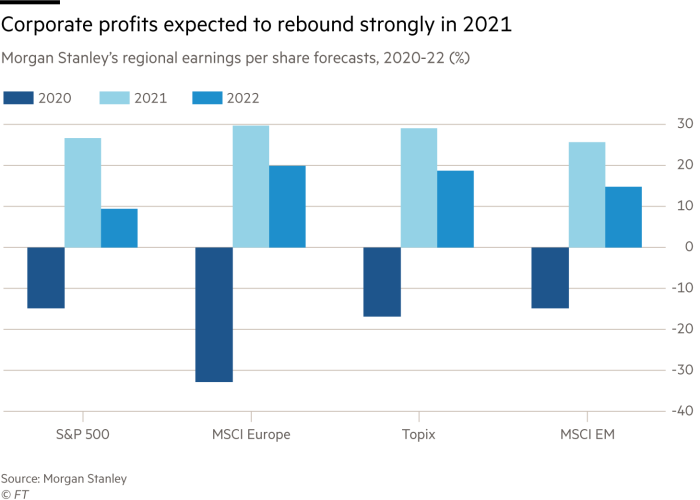

Reports of corporate profits rebounding have reinforced the optimism. And to cap it off, last week it emerged that Mr Biden would name former Federal Reserve chair Janet Yellen as his Treasury secretary. That raises the prospect of co-ordinated and aggressive fiscal-monetary policymaking to combat the economic damage wreaked by Covid-19, further delighting investors.

Ed Yardeni of Yardeni Research referred to Ms Yellen as the “Fairy Godmother of the Bull Market” when she was chair of the central bank in 2014-18, due to her dovish views, and reckons her re-emergence as an influential policymaker is another positive sign for equities. “Now as Biden’s Treasury secretary, she will continue to wave her magic wand,” he argues.

The combination of factors has been electrifying. Fund managers have not been as hopeful that economic growth and corporate profits will improve since 2002, according to a widely-followed Bank of America survey. Their cash reserves have dropped by 1.8 percentage points in the past seven months — the fastest slump on record — to nearly 4 per cent. The survey showed that fund managers’ optimism on stocks has jumped to the highest since early 2018, when markets were basking in the glow of Mr Trump’s corporate tax cuts.

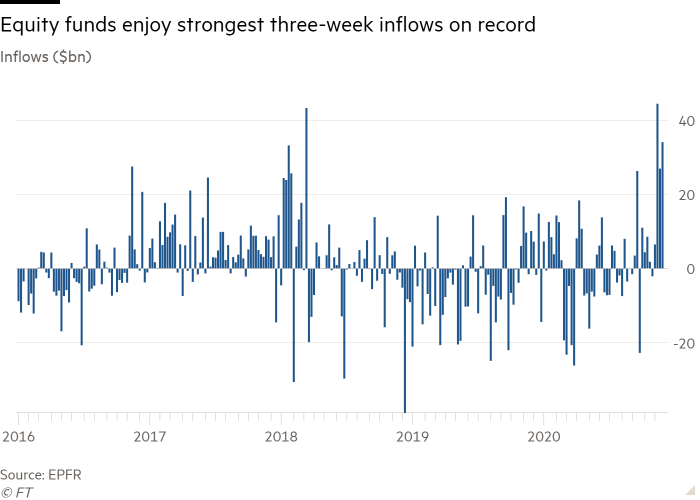

Investors are also pumping more money into fund managers. Equity funds have globally hauled in nearly $90bn since the beginning of November, after the strongest three-week stretch of inflows on record. Goldman Sachs estimates that “short” positioning on US stocks — bets on them falling — is the lowest since at least 2004.

“The vaccines have cemented the view that even if we’re still in a tunnel, there is light at the end of it,” says Liz Ann Sonders, chief investment strategist at Charles Schwab. “The froth in sentiment had been concentrated in day traders, but since the Pfizer news we have seen that frothiness has moved out into pretty much every measure of sentiment.”

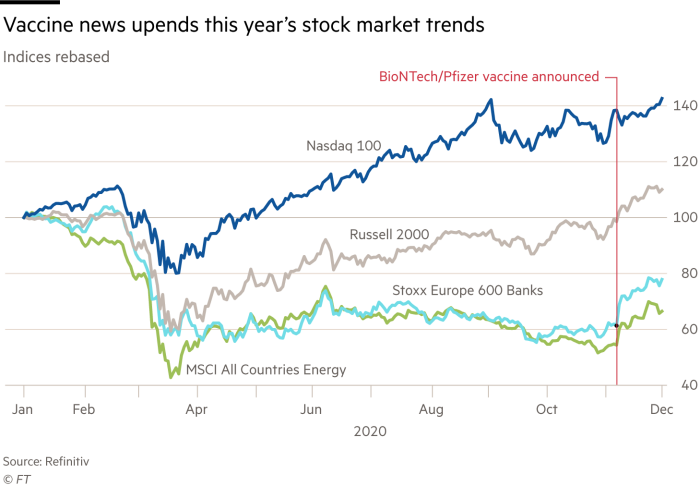

Aside from propelling many major equity market indices to record highs, the November newsflow has triggered a seismic investor “rotation” away from stocks that were seen as Covid-era winners and into beaten-up industries that are more closely tied to the health of the global economy. What was once a one-engine rally — with Big Tech providing virtually all of the vim — has seen markets fire on almost every cylinder in November.

European bank shares and global energy stocks had lost about half their value by the March nadir, and have since largely languished. But in November they soared 30 per cent and 35 per cent respectively. Airline stocks jumped more than 30 per cent. The Russell 2000 index of small US companies climbed more than 18 per cent, almost twice the gain of its “big brothers”, the S&P 500 and the Nasdaq 100 indices. Emerging market stocks rose more than 9 per cent in November, the biggest monthly gain in nearly four years. Junk bonds have almost clawed back all their 2020 losses.

- Retail and institutional investors are helping prop up one of the most remarkable bull runs in financial history during Covid-19 with the emergence of several vaccines.

- Other factors adding to the optimism include lax monetary policy, a Biden win, and potential gridlock.

- Further, Janet Yellen being named Treasury secretary raises the potential for aggressive fiscal and monetary policy.

- But the markets may be ignoring potential red flags as the virus's second wave takes shape and Democrats potentially take the senate.

The markets have become too hot to handle. So intense is the frenzied stock-buying that even many of Wall Street’s biggest brokerages and wealth managers are struggling to keep up.

Almost every major US brokerage firm — from old stalwarts like Charles Schwab and Merrill Lynch to new platforms such as Robinhood — suffered at least one outage in November, according to Downdetector, a website that tracks online service problems, as a torrent of trading overwhelmed their websites.

Thomas Peterffy, the billionaire founder of Interactive Brokers, who first started trading on the now-defunct American Stock Exchange in the 1970s, says the current environment is unlike anything he has ever seen before — but understandable. “Money is now so easy, why not borrow what you can and put it into stocks? That’s what our customers are doing, and they’re making helluva lot of money,” he says.

Retail investors led the dramatic equity market recovery from the Covid-19 shock, flooding internet message boards to share memes, boast of wins and lament losses. But now they are increasingly joined by the investment industry’s heavyweights, which are helping reinforce and broaden out the most remarkable bull run in financial history.

The MSCI All-Country World index climbed another 12.2 per cent in November — its best month on record — to touch new all-time highs. The gauge has added $30tn in market capitalisation since the March lows.

Moreover, this stage of the rally has been mainly powered by corners of the market largely left behind during the pandemic, such as energy stocks, airlines, hotel groups, European banks, smaller US companies and emerging markets. Indeed, it has become what some analysts have termed an “everything rally”, with junk bonds, copper, oil and even bitcoin climbing sharply. The only major markets to have taken a hit are classic havens, such as US Treasuries and gold.

The backdrop to such a frenzy seems improbable. The second coronavirus wave is unravelling some of the tentative economic recovery from the brutal March shock. All told, the global economy is likely to shrink 4.4 per cent this year, according to the IMF — a decline not seen since the Great Depression.

However, the emergence of several credible, effective coronavirus vaccines has triggered a burst of optimism that the global economy is poised for a powerful rebound in 2021, as the pandemic recedes but the extraordinarily aggressive stimulus measures continue to send money sloshing around the financial system.

“The game-changer was the vaccine,” says Peter Oppenheimer, chief global equity strategist at Goldman Sachs. “Hope is one thing, actually seeing the evidence (of a vaccine) is quite another. And the evidence was much better than most people were expecting. We’re still optimistic that you’ll see quite good returns in equity markets next year.”

However, some investors and analysts remain uneasy about the current ebullience. Yes, effective vaccines could eventually suppress Covid-19, but for now it continues to linger and the monstrous damage it has already inflicted will take a long time to heal.

Noting signs of uncritical optimism among fund managers, Bank of America’s chief investment strategist Michael Hartnett recommends that investors ratchet back their exposure to stocks in the coming weeks and months, arguing markets are now approaching a “full bull” stage and are vulnerable to a setback.

Jeremy Grantham, the famed contrarian founder of the investment group GMO, thinks even this is optimistic. He reckons markets have smashed past the “full bull” stage and are in a late-bubble “melt-up” phase that rivals the two biggest bubbles of the past century.

“There is as much craziness now as there was in late 1999 or 1929,” he argues. “It is bewildering, impressive and for financial historians like me, exciting. This is the real thing . . . It looked like we were in a bubble mode this summer, but the real craziness has come out in the last few months.”

Magic wands

The early stage of the rally was powered by mammoth fiscal and monetary stimulus packages from central banks and governments around the world, totalling trillions of dollars. The impact of ultra-easy monetary policy including very low interest rates — and the prospect of it continuing for years to come — remains the dominant driver, analysts say.

But November’s shift from optimism to near-euphoria has been triggered by an alignment of several stars. First, Joe Biden won the US presidency but Democrats failed to gain control of the Senate. For many investors that was close to the perfect result, ejecting the erratic, norm-shattering Donald Trump but stymieing the more radical parts of the Democratic agenda — such as heavy corporate tax increases.

While another big dose of fiscal stimulus may be trickier to pass, this will mean that the Federal Reserve is more likely to keep its foot on the monetary pedal. “Gridlock is Goldilocks,” was the pithy title of one Wall Street analyst’s note on the subject. That President Donald Trump’s refusal to accept the result has failed to trigger any significant unrest has added to investors’ relief.

Then, BioNTech-Pfizer, Moderna and Oxford university-AstraZeneca announced that they had developed coronavirus vaccines that were in most cases more effective than expected. This provided an enormous jolt to global markets, which could contemplate a gradual economic normalisation next year, with pent-up demand and super-easy monetary policy fuelling a huge growth spurt.

Reports of corporate profits rebounding have reinforced the optimism. And to cap it off, last week it emerged that Mr Biden would name former Federal Reserve chair Janet Yellen as his Treasury secretary. That raises the prospect of co-ordinated and aggressive fiscal-monetary policymaking to combat the economic damage wreaked by Covid-19, further delighting investors.

Ed Yardeni of Yardeni Research referred to Ms Yellen as the “Fairy Godmother of the Bull Market” when she was chair of the central bank in 2014-18, due to her dovish views, and reckons her re-emergence as an influential policymaker is another positive sign for equities. “Now as Biden’s Treasury secretary, she will continue to wave her magic wand,” he argues.

The combination of factors has been electrifying. Fund managers have not been as hopeful that economic growth and corporate profits will improve since 2002, according to a widely-followed Bank of America survey. Their cash reserves have dropped by 1.8 percentage points in the past seven months — the fastest slump on record — to nearly 4 per cent. The survey showed that fund managers’ optimism on stocks has jumped to the highest since early 2018, when markets were basking in the glow of Mr Trump’s corporate tax cuts.

Investors are also pumping more money into fund managers. Equity funds have globally hauled in nearly $90bn since the beginning of November, after the strongest three-week stretch of inflows on record. Goldman Sachs estimates that “short” positioning on US stocks — bets on them falling — is the lowest since at least 2004.

“The vaccines have cemented the view that even if we’re still in a tunnel, there is light at the end of it,” says Liz Ann Sonders, chief investment strategist at Charles Schwab. “The froth in sentiment had been concentrated in day traders, but since the Pfizer news we have seen that frothiness has moved out into pretty much every measure of sentiment.”

Aside from propelling many major equity market indices to record highs, the November newsflow has triggered a seismic investor “rotation” away from stocks that were seen as Covid-era winners and into beaten-up industries that are more closely tied to the health of the global economy. What was once a one-engine rally — with Big Tech providing virtually all of the vim — has seen markets fire on almost every cylinder in November.

European bank shares and global energy stocks had lost about half their value by the March nadir, and have since largely languished. But in November they soared 30 per cent and 35 per cent respectively. Airline stocks jumped more than 30 per cent. The Russell 2000 index of small US companies climbed more than 18 per cent, almost twice the gain of its “big brothers”, the S&P 500 and the Nasdaq 100 indices. Emerging market stocks rose more than 9 per cent in November, the biggest monthly gain in nearly four years. Junk bonds have almost clawed back all their 2020 losses.