THEANGEL&THEGAMBLER

Rookie

https://gallery.mailchimp.com/bf2b9b3cf3fdd8861943fca2f/files/Umbrellas_Dont_Make_It_Rain8.pdf

America prides itself on a long-standing belief that anyone can make it financially by working hard and tugging on their proverbial boot-straps. According to a 2014 Pew Research survey, 57 percent of Americans disagree with the statement “(s)uccess in life is pretty much determined by forces outside our control.”But America1 From the pioneers to the financiers, wealthy Americans are acclaimed as self-made men (and on occasion self-made women), succeeding on pure grit, gumption, and ingenuity. ’s egalitarian promise of opportunity and individual agency remains unfulfilled.3 An analysis of who holds America’s wealth makes clear how life outcomes can diverge radically, in particular for those subject to systemic historically rooted discrimination, which is not related to the amount of personal effort exerted.

A comprehensive understanding of wealth – the value of what you own minus what you owe – demonstrates how vulnerability to economic calamity like the Great Recession can have vastly different consequences. Differences in wealth accumulation are important to examine because wealth – whether invested in a debt-free education, small business creation, housing or retirement savings – generates opportunity and improves well-being. In addition, wealth provides the freedom to innovate. Starting a business, inventing a new product, making land productive, attending vocational training, and making investments all beget greater wealth – but they require liquid wealth to get started. In sum, wealth provides people with initial capital to purchase an appreciating asset, which in turn, iteratively generates more wealth. Accumulated wealth can also be passed on to children, begetting yet more wealth and opportunity in an intergenerational manner.

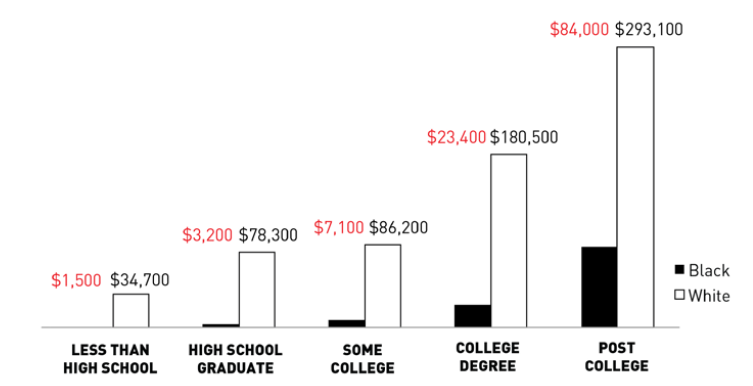

Research and public policy have traditionally focused on education and income as drivers of upward mobility. There is compelling evidence, however, that education alone does little to explain the source of different levels of economic well-being, especially across race. Observing an association between higher levels of educational attainment and higher levels of net wealth and concluding that education produces wealth is tantamount to observing an association between the presence of umbrellas during rainfalls and concluding that umbrellas cause the rain. It is more likely that the relative wealth of different races explains the educational attainment differences across race groups.

For black families and other families of color, studying and working hard is not associated with the same levels of wealth amassed among whites. Black families whose heads graduated from college have about 33 percent less wealth than white families whose heads dropped out of high school. The poorest white families—those in the bottom quintile of the income distribution—have slightly more wealth than black families in the middle quintiles of the income distribution. The average black household would have to save 100 percent of their income for three consecutive years to overcome the obstacles to wealth parity by dint of their own savings activity.6

It is the unearned birthright of inheritance or other family transfers that has the greatest effect on wealth accumulation, and likewise is the largest factor erecting barriers to wealth accumulation for people of color. White families have had significantly more time to pass

These generational transfers include financing their children’s college education, giving them down payments for houses, and more generally providing them with inheritance and other gifts to seed asset accumulation. Intergenerational transfers are central sources of wealth building. Black families, however, have never had comparable resources to pass down to succeeding generations. As such, black families whose members study and work hard are still hindered in their efforts to generate the resources necessary for their own security and to ensure the well-being of their children