Hit dogs holler. And the degree of moral grandstanding you engage in doesn't line up with simple adaption.

All I do is advise people to avoid serious debt and save / invest a decent portion of their income.

That's good advice, but 2 things.'

All I do is advise people to avoid serious debt and save / invest a decent portion of their income.

So the generation that fukked future generations of Americans also fukked themselves.

Here’s the thing in my perfect world.....That's good advice, but 2 things.

1. Avoiding debt is difficult for most people that aren't lucky enough to have a financial support system.

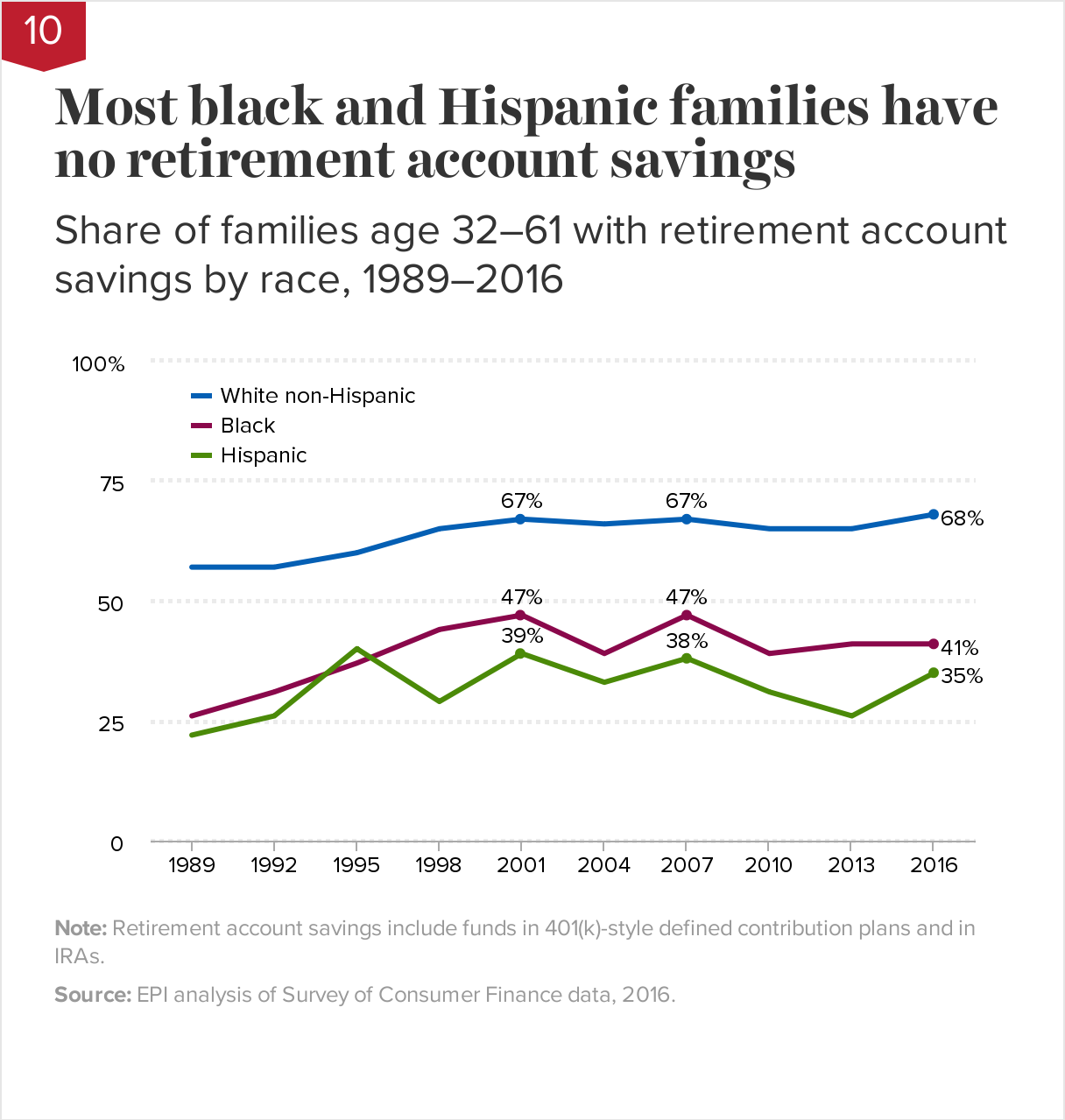

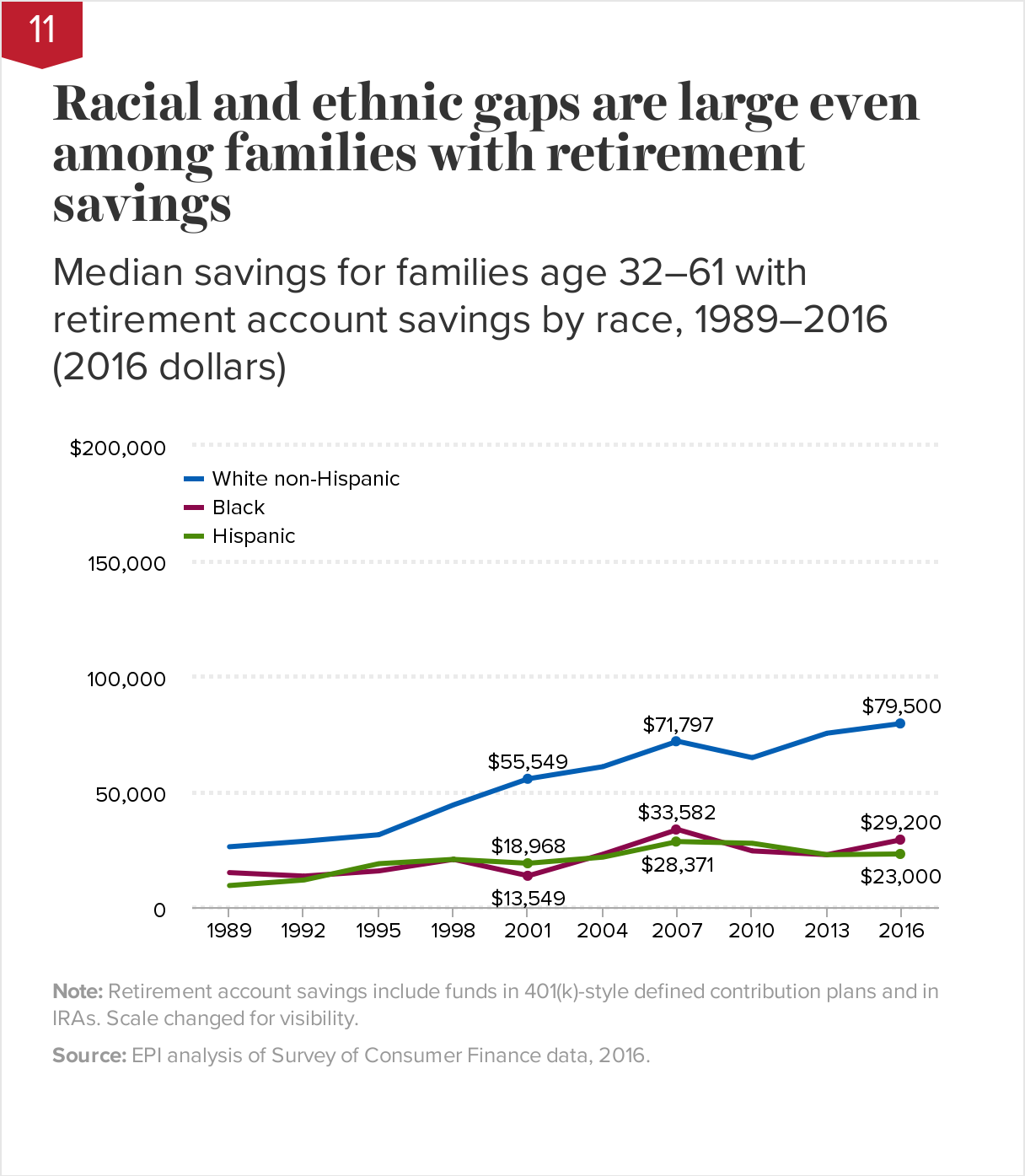

2. 78% of Americans were living paycheck to paycheck before Covid-19. So, at least that many Americans have had to use more than a "decent portion" of their income just to survive. When 4/5 people are living check-to-check, there's no extra money to invest.

And in 2021 when we see the real economic effects of this pandemic? Most people can kiss that 'decent portion of their income to invest' notion goodbye.

EDIT I guess if you mean boomers they do have more money for this

So the generation that fukked future generations of Americans also fukked themselves.

yall nikkas give me shyt all the time for the stuff I say, but how is it any different from any other financial educator:

That's good advice, but 2 things.

1. Avoiding debt is difficult for most people that aren't lucky enough to have a financial support system.

2. 78% of Americans were living paycheck to paycheck before Covid-19. So, at least that many Americans have had to use more than a "decent portion" of their income just to survive. When 4/5 people are living check-to-check, there's no extra money to invest.

And in 2021 when we see the real economic effects of this pandemic? Most people can kiss that 'decent portion of their income to invest' notion goodbye.

EDIT I guess if you mean boomers they do have more money for this

You'd think I was saying take out 35% payday loan or cop a dodge challenger / hellicat at 0 down with 40% interest.Anything short of a full throated rebuke of the system will usually have people complaining about what you post.

Take it in stride.

That has nothing to do with it. He routinely says he has “no remorse” and gives the problem 2 seconds and spends 90 percent of the time just concern trolling and lecturing to people about responsibility. He always highlights the most extreme examples and ignores systemic problems or feigns like he cares while arguing as if they don’t exist. It’s like those dudes on the Intercept who claim to be anti-racist but go and do field interviews and some how always find the what about black on black crime guy when a black dude gets shot. To top it all off he is talking to people from rougher upbringings than him who watched their parents do what he does by choice as a necessity. It will never play well. Serious literally says shyt all the rest of us always say like @ogc163 but then we spend most of our time trying to discuss systemic problems because the rest of it is so common sense that we don’t feel like it needs to be discussed as nauseum but he’s nowhere to be found in those sorts of discussions. He just shows up regurgitating 101 level shyt and thinks he’s bringing some novel “tough perspective.” In his own mind he is bringing an opposite perspective than us “excuse makers” except he isn’t actually disagreeing with anything or presenting anything new. Look @ his last post - state a bunch of generic leftist points and then go back to his bootstraps shyt not realizing that there’s an inherent disconnect between the two forms of argumentation. One accepts human error and frailty and seeks to mitigate it by creating a society where the baseline for how far you can fall is much higher and the other assumes a world where the options and choices are clear and distinct and it is merely a matter of having the proper judgment to choose them. The tough decisions he talks about have to be made precisely because of the world as it is designed - so wouldn’t it be more prudent to spend more time on how to eliminate that system, which is a much tougher question? We can go ahead and have a finance 101 thread - he brings that shyt where it doesn’t belong and people have grown tired. And then @ people like me who literally spent his entire tenure as moderator creating college and grad school threads designed to inform people and encourage them to make smart financial decisions. No one knows what the fukk he be on but we like him too much to say anything.Anything short of a full throated rebuke of the system will usually have people complaining about what you post.

Take it in stride.