Average U.S. Checking Account Balance 2017: A Demographic Breakdown

According to data from the 2013 Federal Reserve Survey of Consumer Finances, the median checking account balance for U.S. households was $2,900, while the average balance was $9,132. The large difference between the two figures was due to the overrepresentation of high-income households in the survey. For a closer look at the amounts people keep in their checking accounts, we turned to figures broken down along several demographic categories.

Average U.S. Checking Account Balance 2017: A Demographic Breakdown

Here's how much cash Americans have been keeping on hand in a checking account. How do you compare?

Maurie Backman

(TMFBookNerd)

Jan 22, 2017 at 9:18AM

We all know we're supposed to save a portion of our earnings for emergencies or the future, and unfortunately, many of us are falling short in that regard. It's estimated that 69% of Americans have less than $1,000 in a savings account, while one in three workers has yet to even start saving money for retirement.

But perhaps our lackluster savings aren't an indication that we're spending too much of our earnings, but rather, that we're putting our money in the wrong place. According to a Federal Reserve study, as of 2013 (the last year for which data is available), the average American family had a checking account balance of $9,132. Not only that, but balances across the board have grown over time. And while having extra money on hand is a good thing in theory, it's a bad move in practice.

Here's what we've been keeping in checking accounts

Americans' checking account balances have largely been growing since 2001. Back then, the average checking account had $6,404. By 2013, that number climbed to $9,132. If these numbers seem high, we can assume that it's partly because the wealthy are bringing up the average. But there's more to it than that.

The following chart summarizes our collective checking habits over a 12-year span:

As you can see, checking account balances climbed between 2001 and 2004, dropped a bit in 2007, and then slowly but surely crept back up for a 12-year high by 2013.

Why the trend? During periods of economic prosperity, many of us are more apt to keep our money invested. When the economy slumps, we tend to pull our money out of the market and keep it someplace safe, like the bank.

Case in point: Over 500,000 jobs were lost in 2002, and unemployment rose from 4.2% in February 2001 to 6.3% in June 2003. Furthermore, 2002 and 2003 were miserable years for the Dow, with the market reaching a record low in March 2003. All of this explains why the average checking account balance rose from $6,404 in 2001 to $7,382 in 2004.

But then things picked up a bit. Unemployment rates dropped by mid-2005, and the Dow climbed from 7,674 in March 2003 to 10,508 by April of that year. And consumers followed suit, letting their checking account balances gradually drop between 2004 and 2007.

Of course, that sense of economic security was only temporary. Once the 2009 economic recession hit, many of us fell back into our former ways, keeping our hard-earned cash close by. And because the recovery from that bout was gradual at best, it's no wonder the average American still had over $9,000 in a checking account four years later. But while there may be some logic behind the decision to overfund a checking account, it's a move that could prove costly in the long run.

Better checking practices

So how much money should you keep in a checking account? As long as you have a savings account with enough money to cover three to six months of living expenses, you really don't need much more than what it takes to pay your bills for the upcoming month.

Although some checking accounts do pay interest, most don't. And although today's savings account rates are nothing to write home about, it's better to earn 1% on your money than nothing at all. If you open a checking and savings account at the same bank, you can generally transfer money between the two instantly and automatically -- so if your savings account has enough money to cover three to six months of living expenses, you should be set. In addition, you should make sure your checking account balance is high enough to prevent your bank from charging a fee, but if you have enough cash to pay for three to six months of bills, you should be more than adequately covered.

Furthermore, as long as you have enough money in savings for emergencies, and enough money in checking to cover your near-term expenses, you should invest your excess cash, rather than let it sit in the bank. Even a relatively conservative investment portfolio can deliver an easy 5% return, which is much higher than what you'll see with a savings or interest-paying checking account.

The effects of checking account overdependency can add up over time. Imagine you house $9,000 in a checking account year over year, $5,000 of which you generally don't touch to pay your bills. If you were to invest that excess $5,000 for 20 years at a 5% return, it would grow to more than $13,000. Better yet, if you were to invest that money in stocks at an average annual return of 8%, you'd have $23,000 two decades later.

Of course, it's better to have extra money in a checking account than to have insufficient cash to pay your bills. But if you put too much in a checking account, you'll lose out on a growth opportunity that could be pivotal in helping you meet your long-term goals.

It's true that a checking account is a zero-risk prospect; the only way for you to lose money is to withdraw it yourself. But despite the fact that the stock market has experienced too many periods of volatility to count, if you're willing to ride out those ups and downs, you'll likely grow your money, rather than letting it rot away interest-free. Between 1965 and 2015, the S&P 500 underwent 27 corrections of 10% or more, but it ultimately recovered from every one. Difficult as it may be to relinquish some control over your finances, if you're willing to be patient and put a little faith in history, you stand a strong chance of coming out much richer in the long run.

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $16,122 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.

A History of the Average American's Checking Account Balance in 1 Chart -- The Motley Fool

The saving accounts shyt they do every year is misleading.

The average Checking Account balance for black people is $2k but the median (most black people) have below $855 if they even have a checking account at all according to the data.

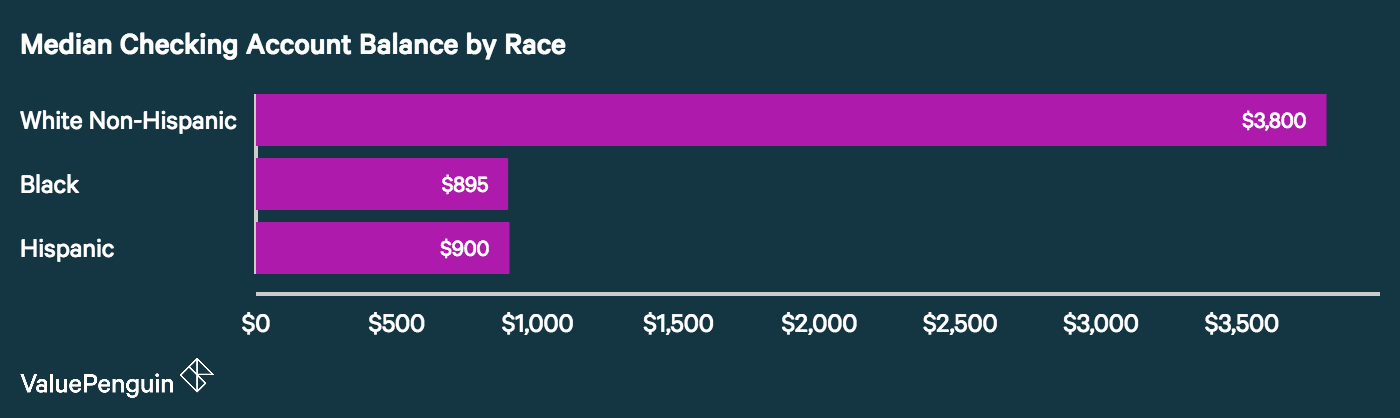

Average Checking Account Balance by Race

The survey also prompted respondents to identify with one of several categories related to race. The data revealed a large difference in checking account balances between white non-Hispanic households and other groups.

Race Average Checking Account Balance

White Non-Hispanic - $10,909

Black - $2,501

Hispanic - $2,730

Both the average and median balance numbers were four times greater for white households than for black and Hispanic households, but there are a number of other facts that may be more useful to understanding the differences involved. First, about 25.5% of black and 21.2% of Hispanic respondents had no checking accounts at all, compared to just 4.78% of white non-Hispanics. These "unbanked" households may keep their funds in cash or other non-deposit assets like prepaid debit cards.

Finally, the large number of high-income participants in the survey may have had an influence on the median checking account balances of the race categories. While white non-Hispanic households accounted for about 71% of all participants in the 2013 SCF, they made up over 89% of households in the highest income bracket. Compounding this imbalance is the overrepresentation of the wealthiest households necessary for the survey's other objectives. These two factors likely resulted in an excessively high median and average for checking account balances.

Average U.S. Checking Account Balance 2017: A Demographic Breakdown

Last edited: