JahFocus CS

Get It How You Get It

Intro:

Excerpt:

Full article

How Obama Destroyed Black Wealth

By Matt Bruenig, Ryan Cooper

The nation's first African-American president was a disaster for black wealth.

Angela Walker (3rd-L) and her daughter Nazarin (2nd-L) listen to local officials speaking on home foreclosures at their home in Suitland, MD in 2010. Walker was being threatened with foreclosure and had sought help from Rev. Jesse Jackson's Rainbow PUSH Coalition. Alex Wong / Getty Images

The Obama presidency was a disaster for middle-class wealth in the United States. Between 2007 and 2016, the average wealth of the bottom 99 percent dropped by $4,500. Over the same period, the average wealth of the top 1 percent rose by $4.9 million.

This drop hit the housing wealth of African Americans particularly hard. Outside of home equity, black wealth recovered its 2007 level by 2016. But average black home equity was still $16,700 lower.

Much of this decline, we will argue, can be laid at the feet of President Obama. His housing policies led directly to millions of families losing their homes. What’s more, Obama had the power — money, legislative tools, and legal leverage — to sharply ameliorate the foreclosure crisis.

He chose not to use it.

Excerpt:

Black Wealth Destroyed

Even before the crash, decades of discriminatory policies had depressed African-Americans’ housing wealth. New Deal federal housing subsidies — the bedrock of the postwar middle class — largely locked out African Americans. Racist housing covenants forbade neighborhoods from selling or renting to black families, back up by the threat of riot. Black families that could buy were often brutally exploited by contract sellers.

The mortgage bubble fostered similar abuses. Originators, looking for anyone to take subprime mortgages, handed them out to disproportionately black lower-class people, and steered black middle-class families who would have qualified for ordinary mortgages into subprime loans as well.

Former Wells Fargo employees later testified that the bank deliberately tricked middle-class black families (who they called “mud people”) into subprime “ghetto loans.” Overall, a Center for Responsible Lending study found that from 2004 to 2008, 6.2 percent of white borrowers with a credit score of 660 and up got subprime mortgages, while 19.3 percent of such Latino borrowers and 21.4 percent of black borrowers did.

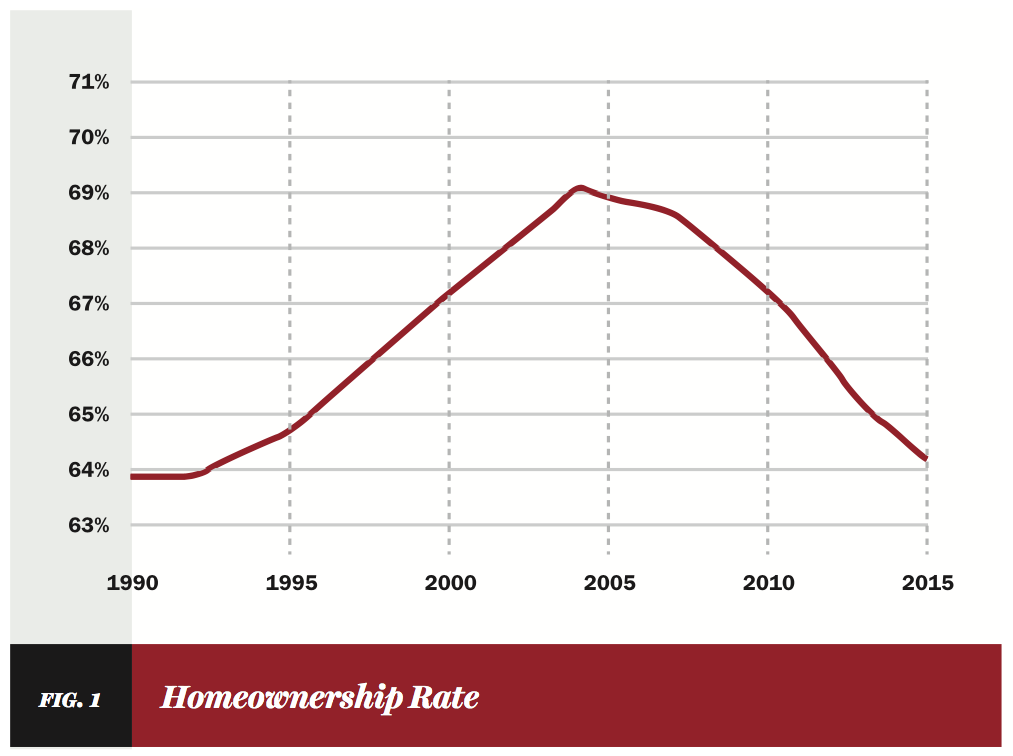

The effects of the foreclosure disaster are starkly apparent in Survey of Consumer Finances data. To start, the homeownership national rate shows a marked decline over almost the whole Obama presidency, reaching the lowest rate since 1965 (before slightly rebounding).

Broken down by race, the overall story for homeownership is similar for all groups, but black homeowners started lower and stayed lower than white ones, with no rebound at all from 2013 to 2016.

However, the total homeownership rate can be misleading in that it includes people with negative equity, which is worse than owning no home at all — it is merely “a rental with debt.” After the crisis, the percentage of black homeowners with negative equity exploded by twenty-fold, from 0.7 percent to 14.2 percent — and unlike white families, did not reach its peak until 2013.

Next we examined home equity by race. Here is average white, black, and Latino home equity by year:

The sharp decline from 2007 to 2013 is readily seen, as well as partial recovery through 2016, and the large racial wealth gap. Average white home equity in 2016 is 3.5 times greater than the same black figure, and it has regained 84 percent of its 2007 value, compared to a black figure of 73 percent.

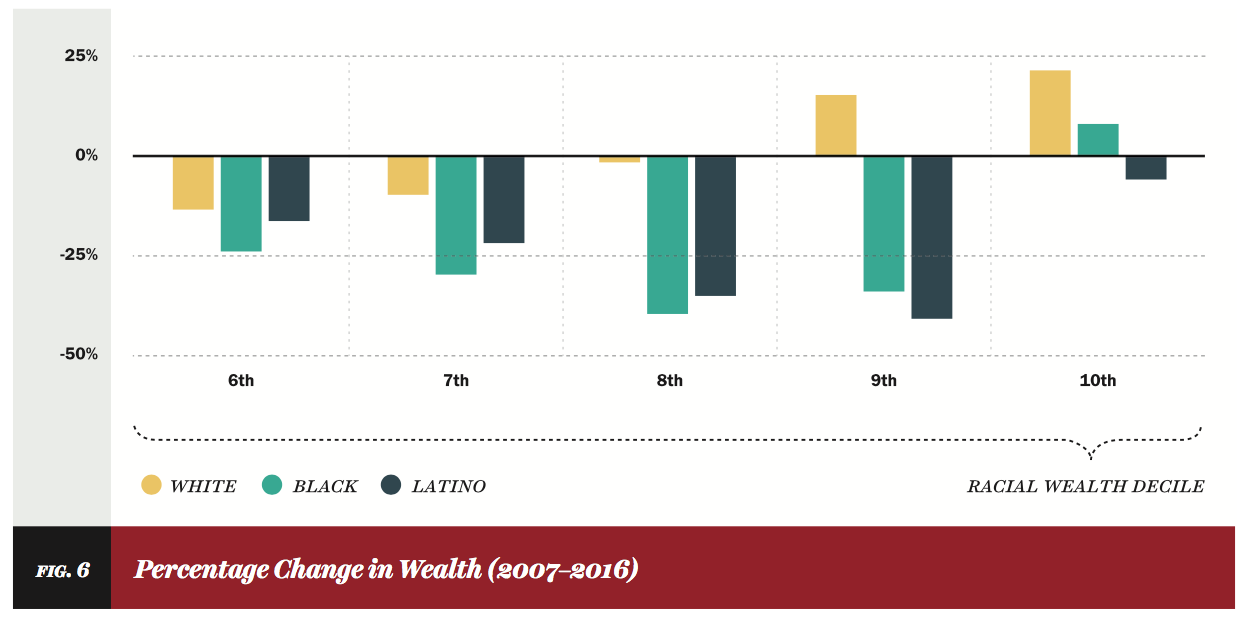

Then there are the distributional effects. Home ownership makes up a much larger percentage of black and Latino wealth than it does white wealth, and a much larger percentage of middle-class wealth than top wealth in all racial groups. On the eve of the recession, middle-class families tended to hold 50 percent to 70 percent of their wealth in home equity, while the wealthiest 10 percent of families held 15 percent to 30 percent of their wealth in home equity.

Given these differences in wealth portfolios, bailing out financial assets after 2008 while allowing homeowners to drown directly concentrated the national wealth into the hands of the richest white families.

Between 2007 and 2016, the wealthiest 10 percent of white families saw their wealth expand by an average of $1.2 million (21.6 percent), the next wealthiest 10 percent of white families increased their net worth by an average of $141,000 (15.5 percent), and the top 10 percent of black families grew their wealth by $78,000 (8 percent). Everyone else experienced wealth declines as high as 40 percent.

Mass foreclosures have severe ripple effects. People who lose their homes are at greater risk of job loss and falling into poverty, and are more likely to commit suicide. Nearby homes lose value, as foreclosed properties are often blighted. A 2013 Center for Responsible Lending study estimated that properties in proximity to a foreclosure shed $2.2 trillion in value — and that half that loss was in communities of color.

The decision to hang homeowners — especially black homeowners — out to dry was a catastrophe.

Full article

at the very low traction this thread has gotten.

at the very low traction this thread has gotten.

Those are the type of Negroes that think the only bad white people are those who’re conservative and/or vote Republican or randomly scream racist rhetoric from a pickup truck or on reddit.

Those are the type of Negroes that think the only bad white people are those who’re conservative and/or vote Republican or randomly scream racist rhetoric from a pickup truck or on reddit.